“If Santa Claus should fail to call, bears may come to Broad and Wall.” – Yale Hirsch

The term “Santa Claus Rally” was coined by Yale Hirsch, author of the “Stock Trader’s Almanac”, and has been referenced by investors for decades. It is defined as the last five trading days of the year (beginning at noon on the sixth day) and the first two of the next year. Historically, this has been the best performing stretch of seven trading days of the year.

Like other popularized Wall Street sayings, the term “Santa Claus Rally” has been conflated by many. Just as the Christmas shopping season starts earlier and earlier every year, commentators start asking if the Rally is going to happen well before it has even begun. The problem is that the first two weeks of December has historically seen stock market under performance. This early-December under performance also leads many to think no Santa Claus Rally will happen the last five trading days have arrived.

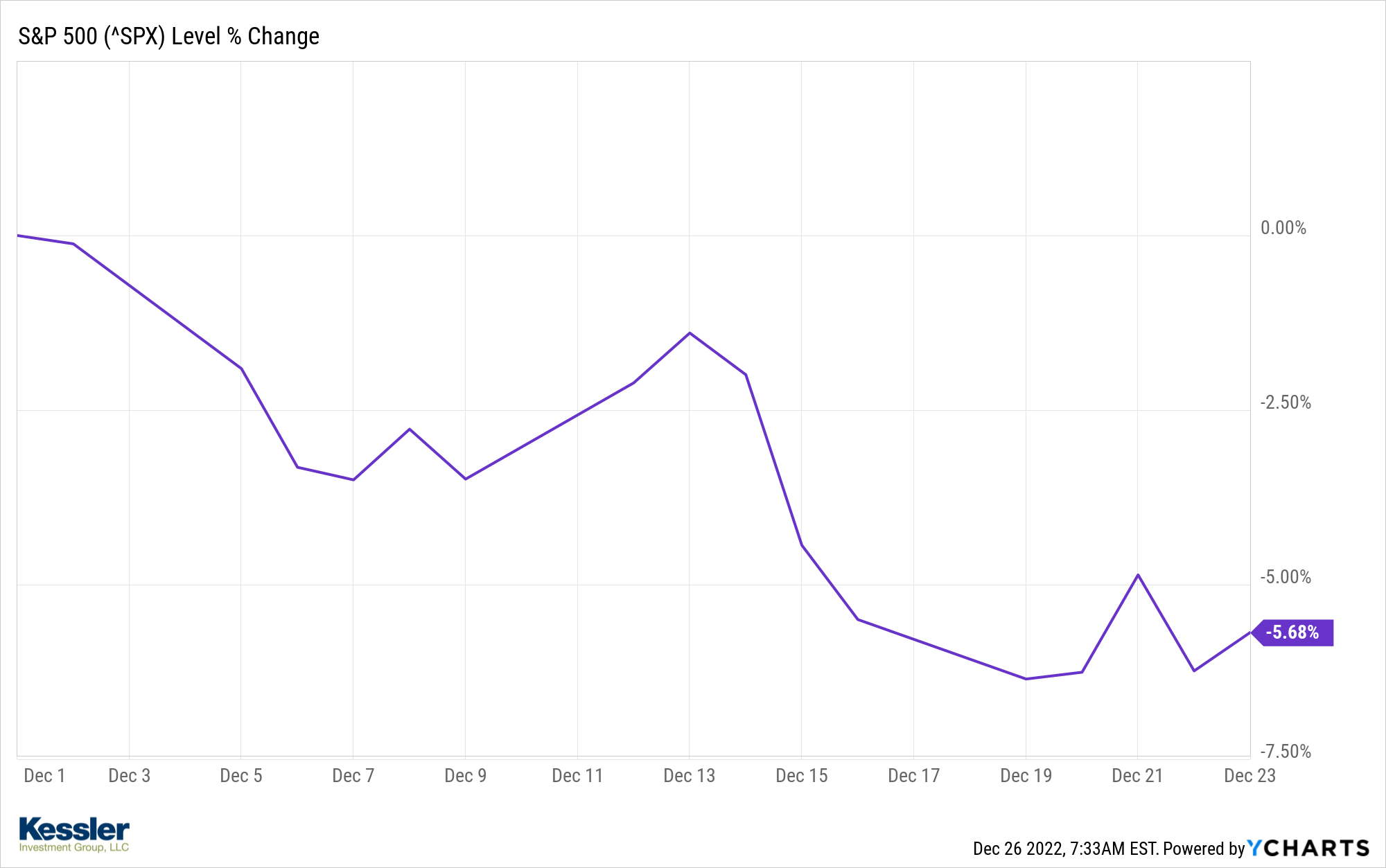

This year’s early-December under performance has done the same thing and led many to declare the Santa Claus Rally over before the final five trading days had even begun! For 2022, the last five trading days began on Friday the 23rd (technically noon on the 22nd.) In the chart below, you can see how 2022 looks so far. It shows how stocks started the month in a downtrend before bouncing around December 22.

So far, the historical norms are holding. The first two weeks of trading days in December saw the S&P 500® Index (“SPX”) decline by approximately 7.7%. Since the period established for the Santa Claus Rally began, the SPX is up approximately 1.9%. We will need to wait until January 4th, 2023, to see how it plays out this year.

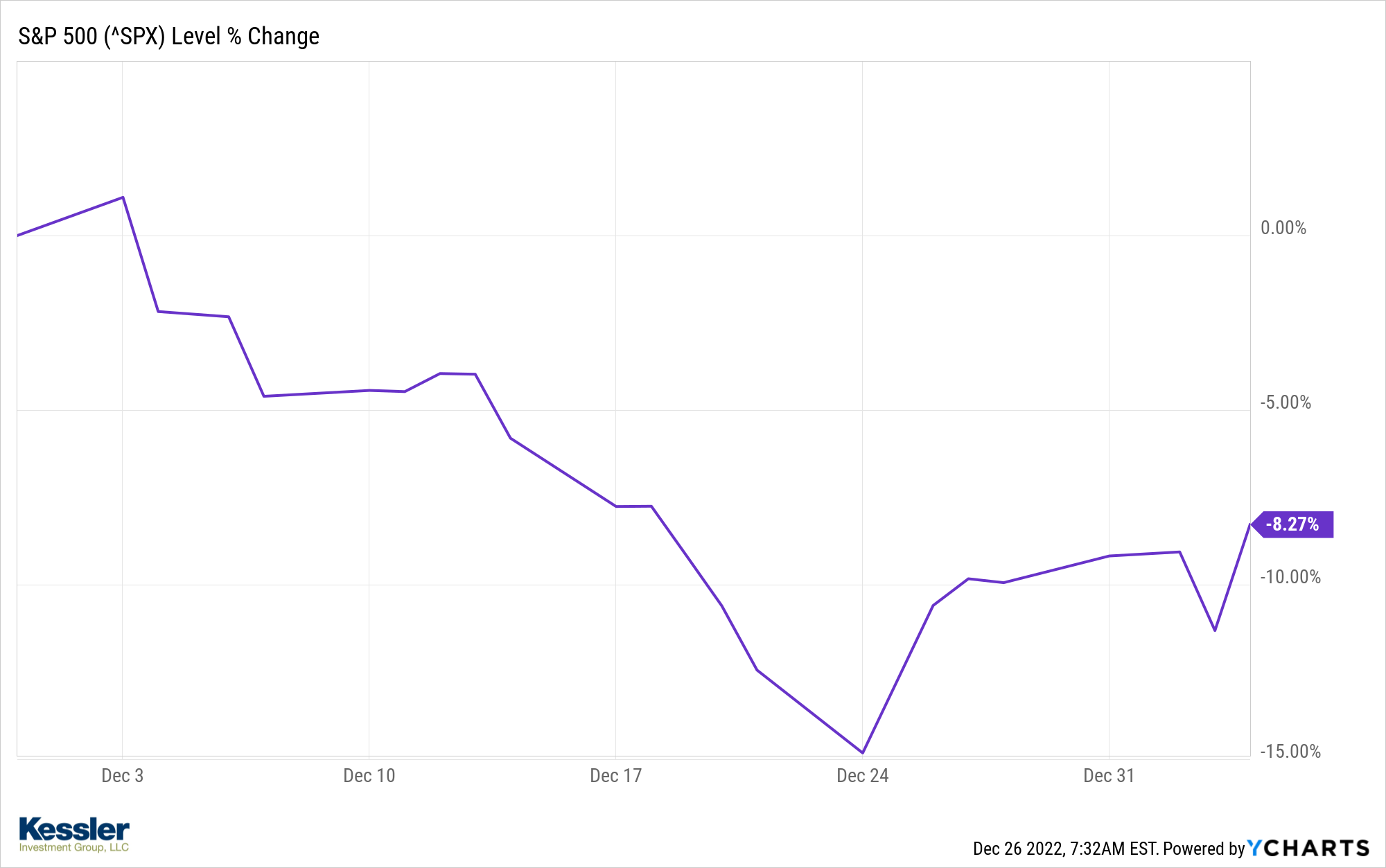

Now let us look at 2018. This is the last time the Federal Reserve raised interest rates and offers another example of the Santa Claus Rally being declared over before it had even begun. The chart below shows how stocks performed in December 2018 and the first few days of January 2019. Take note of how similar the two charts appear. The SPX declined until Christmas Eve when the Santa Claus Rally began and delivered approximately a 7.7% boost that year.

While past performance does not predict future results, it can be helpful to our understanding of investor behavior. Negative sentiment can take hold and lead investors to grow progressively more bearish in their outlook for the future. This continues until all the “sellers” are done selling which leaves the “buyers” to dictate the direction of the market. Effectively, this is what we believe happens leading up to the Santa Claus Rally. It is also worth noting that the same phenomenon can happen in reverse. We see this when enthusiasm drives bullish activity until everyone who wants to buy has done so, leaving only the sellers to dictate the direction of the market. These cycles can occur over very short periods or, indeed, over many years.

So, while we are not necessary calling for a dramatic rally in 2023, it is worth looking at how stocks performed in the year following the last Fed rate hike cycle. Of course, there are obvious differences between 2018 and 2022 in terms of inflation, the economy, and politics. However, this is usually true when comparing any two periods. Below is a look at the SPX for 2019 which followed a 20% decline to end 2018….and a Santa Claus Rally.

As you can see, stocks had a strong year of performance in 2019. We will need to wait and see if something similar is in store for 2023.

Now we want to outline the issues we think will influence markets in 2023. As is always the case here at KIG, when market conditions change, we do our best to adjust to these changes. While we believe in investing for the long term, this does not mean we simply buy and hold investments without regard for these changes. Here is our take on the factors we think will dictate performance in 2023.

Even those who have lived under a rock during 2022 are likely to know that inflation is back. We have spent a lot of time over the last decade discussing how the Federal Reserve has been battling DEFLATION since the Great Financial Crisis (“GFC”). We have also pointed to our view that deflation and inflation are two sides of the same coin. Neither inflation nor deflation are good for the economy, but deflation is more dangerous and difficult to manage.

Since the GFC, the Fed has been alone in battling deflation. With only one tool (interest rates), to battle deflation, the Fed has barely been able to keep deflation at bay. Congress, on the other hand, has done little to help the Fed with their policy tools, also known as fiscal policy. In March of 2020, things changed when both fiscal and monetary policy came together in response to the COVID shutdown.

In a similar way to the effect World War 2 had on the Depression (another period plagued by deflation), the government’s coordinated response to COVID broke the back of deflation. Ignoring all the political rhetoric, we see the inflation currently at hand as the natural byproduct from the demise of deflation.

We believe the Fed is prefers battling inflation rather than deflation. Monetary policy is a more effective tool against inflation than it is against deflation. Also of importance to the Fed is to have the ability to move rates lower to combat future economic downturns. The tradeoff is that we must experience the negative effects of a slowing economy to get there.

The Fed has two mandates. They are Price Stability (low inflation) and Full Employment. These mandates are difficult to manage at the same time when inflation is rising and unemployment is rising, too. This happened during the late 1970’s and early 1980’s. Then Fed Chairman Volker decided to fight inflation despite the effect of higher unemployment. At the time, he was vilified for putting the economy ahead of workers who were laid off as growth slowed. Today, he is credited with doing what was right versus what was popular. We will have to wait and see if history is also kinder to Chairman Powell than his contemporaries.

The Fed has been surprisingly aggressive at raising rates in 2022. With unemployment remaining low, it has used this cover to attack inflation before unemployment starts to increase. Volker had no such luck as he had to battle inflation and unemployment at the same time (Stagflation).

The Fed will continue to fight inflation until unemployment rises to around 4-5%. If successful, the Fed will be able to soften interest rates to help boost the economy without the risk of inflation re-igniting. We expect the Fed to do exactly this at some point in 2023. That is, they will be able to back away from rate hikes and turn their attention to stimulating the economy to avoid higher unemployment. The only question is whether we enter a recession in the meantime.

We called for a 2023 recession in our January 2022 letter to clients. While we did not expect a recession in 2022, we also did not expect the Fed to raise rates this aggressively. While we could still be right about a 2023 recession, that view has become popular. Ed Yardeni, the famed market strategist, recently commented, “A recession next year would be the most widely anticipated downturn on record.” We agree that it is difficult to find anyone who things the economy will avoid recession in 2023.

It is part of our nature to be contrarian. With a recession so widely expected, it is difficult for us to continue with the view that a recession comes in 2023. Maybe it does, but economic growth remains persistent. It is this growth that brings down the odds of a recession next year.

Our outlook for inflation is constructive for 2023. We expect the rate of inflation to continue its decline. Will it reach the 2.5% target set out by the Fed? It is unlikely that we see this level of inflation, but it should not be ruled out. After all, the early indicators of inflation from a year ago have reversed course in a significant way. As these prices from earlier in the year come off the boil, inflation will be pulled down too.

Wage inflation, however, is a concern of the Fed and for us, too. For the Fed to feel comfortable with softening their position on rate hikes, wages need to come down. A drop in wage inflation is usually accompanied by an increase in layoffs. To manage inflation without causing unemployment requires surgical precision. Unfortunately, the Fed’s scalpel comes in the form of the sledgehammer that is interest rate policy.

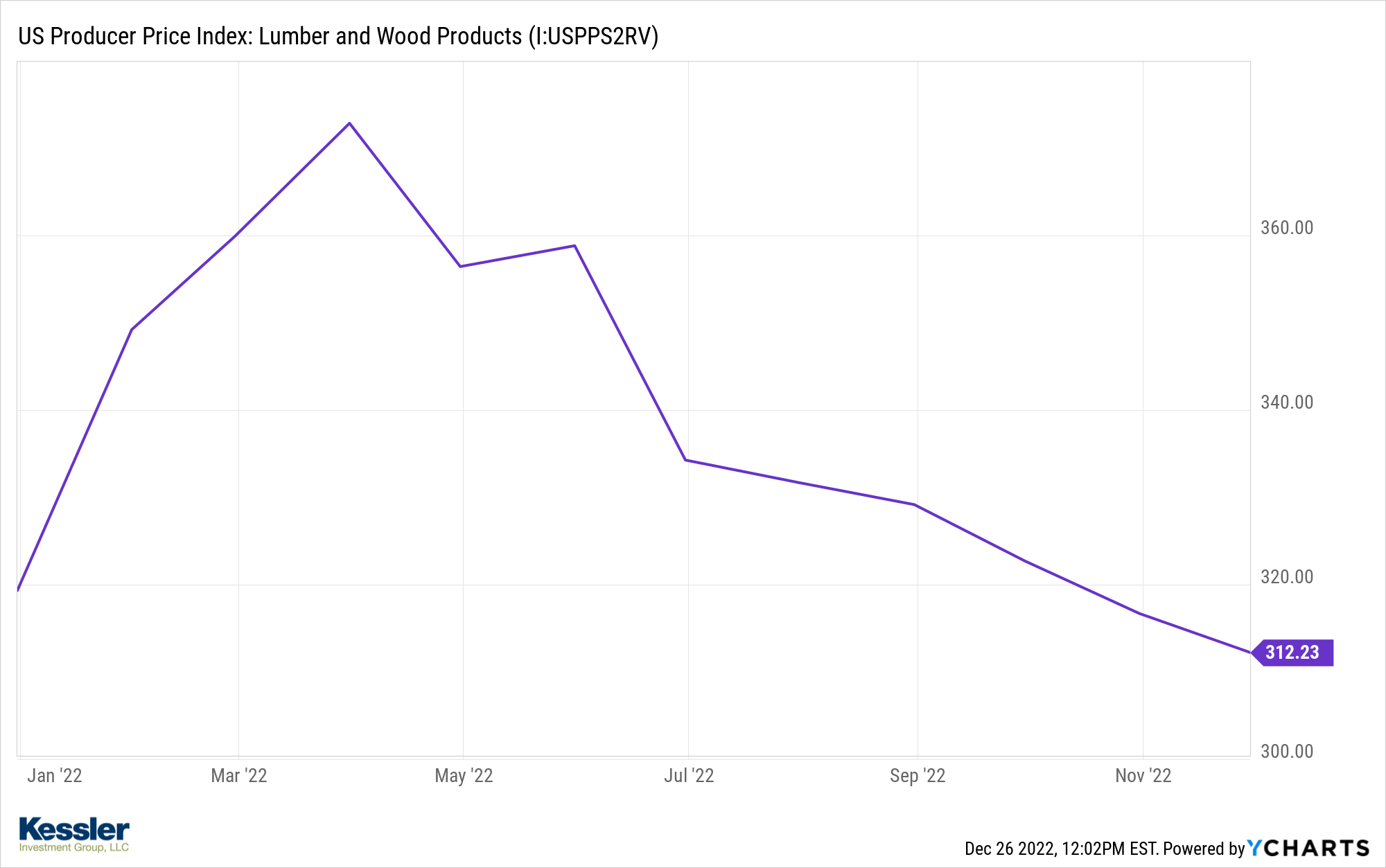

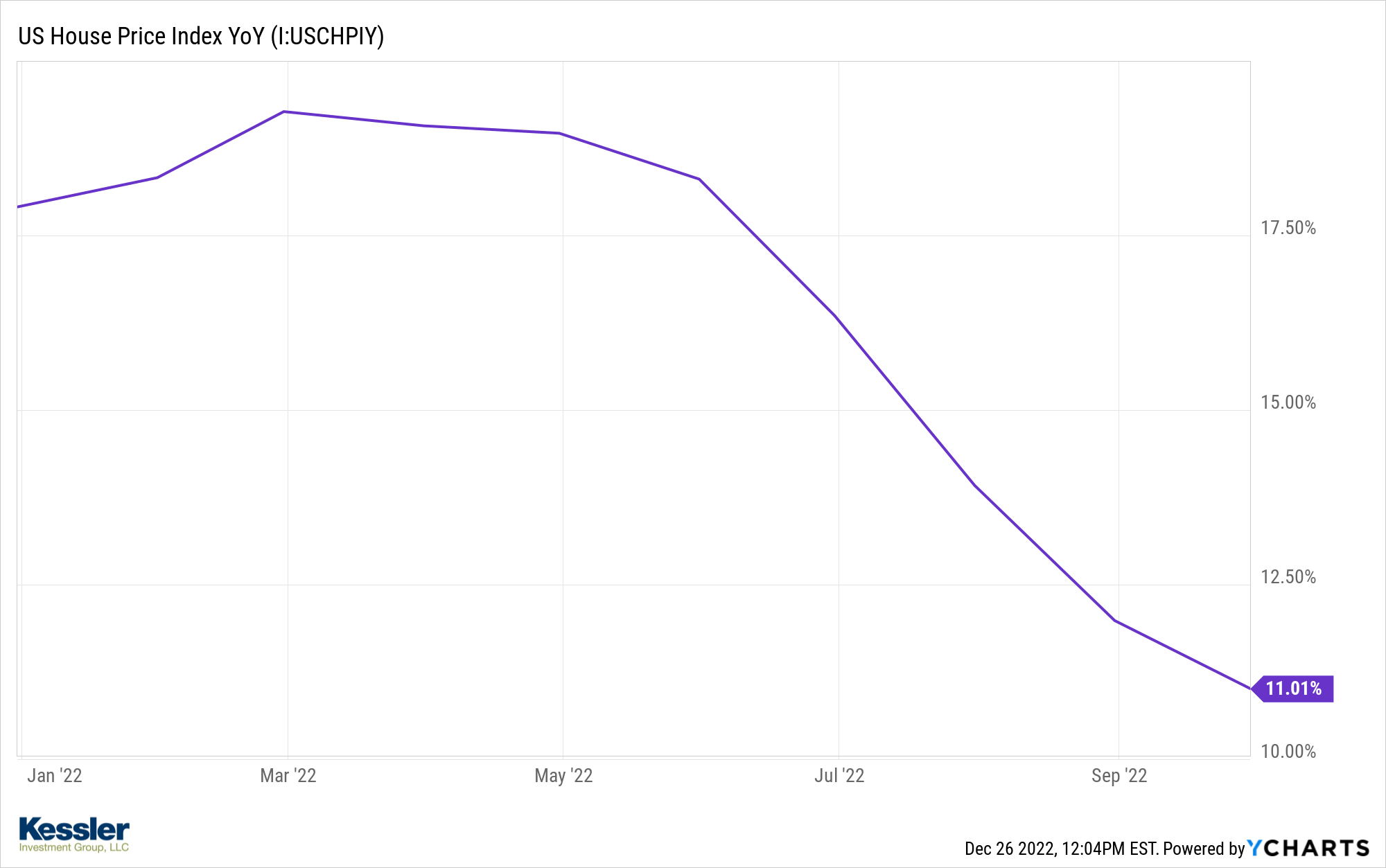

The charts below illustrate how oil, lumber, used cars, and home prices have rolled over. Since the effect of rate hikes from the Fed usually lags by 6-9 months, we have yet to feel the impact of the four 75 basis point hikes that happened in the last half of the year. We expect the effect of these hikes to be felt in the first half of 2023. Therefore, we do not expect inflation be the threat in 2023 that it was in 2022.

Earnings

The popular view today is that stocks will decline further in 2023 as corporate earnings come down. Despite rising inflation, rising interest rates and global turmoil, corporate earnings have remained mostly above expectations. Strategists contend that analysts have not lowered their outlook for corporate earnings to account for the slowing economy that lies ahead. Maybe. Then again, we never want to underestimate the ability of U.S. companies to squeeze out profits in tough environments.

As we have said before, the two cohorts we have the most faith and confidence in is business owners and U.S. consumers. Not politicians or government bureaucrats. Business owners wake up every day and figure out how to carve out profits regardless of the environment. Consumers wake up and look for something on which to spend their money. We think the resilience of these two groups will soften the blow of higher interest rates on corporate earnings.

Nevertheless, we are concerned that higher interest rates will decrease the earnings multiple investors are willing to pay for those profits. After all, as interest rates rise, they act as competition for stocks. The days of TINA (There Is No Alternative) is gone for stocks. Indeed, investors do have an alternative and it is in the form of higher interest rates on bonds.

We think that the impact of lower earnings will not be felt across the board. Sectors like Materials, Industrials, Energy and Healthcare could see a boost to their earnings. Technology, Consumer Staples, Real Estate and Financials could see the opposite.

Here at KIG, it is our goal to allocate the precious savings entrusted to us by clients to those sectors that might benefit from the winds of change ahead in 2023. We expect to maintain an overweight in Energy while increasing our exposure to Healthcare, Industrial and Materials stocks. We expect to decrease our exposure to banks. We have not had exposure to Real Estate or Consumer Staples.

Interest Rates

We touched on interest rates above in our comments about inflation. However, we want to offer our thoughts what the Fed is likely to do when it comes to interest rate policy.

Twenty-twenty two was the worst year for bonds in a generation. We have never seen bonds and stocks perform so poorly in the same year as we did this year. Do not expect the same to happen in 2023 even if stocks slip further. Bonds represent compelling value to us. It has been years since we have felt this way. For our managed accounts that are oriented toward bonds, we are finally finding good yields to lock in.

With inflation likely continuing to come down, we think the pressure on the Fed to keep pressing harder on the economic brakes will lessen. We agree with the consensus that the Fed will raise rates again at their Jan/Feb meeting. Will it be 25 or 50 bps is the popular question and one we do not have a strong feeling about. What we think is important is that the Fed will continue to hike until they see signs that they are breaking the economy. They are not as concerned about a recession as they are a spike in unemployment.

A recession like the one in 1990 would do the Fed just fine. During the 1990 recession, the spike in unemployment came at the very end. It was also a recession characterized by a lack of hiring more than an increase in firing. This is precisely what we have been calling for over the past year and think it will describe the impending recession whenever it might come.

This Fed has shown itself to be willing to switch gears from hiking to cutting rates in short order. It did just that between the end of 2018 and the beginning of 2019. In December of 2018, the Fed clearly set expectations for multiple rate hikes in 2019. By the end of 2019 not only had the Fed not raised interest rates but they cut them three times. The “experts” might be sure that the Fed keeps hiking interest rates through 2023, but we are less sure that this will be the case.

Before we move on from rates, we would be remiss if we did not mention the inversion of the yield curve. Simply put, when short term interest rates exceed long term interest rates, the yield curve is said to be inverted. History suggests that when this happens, a recession will follow. We agree with this view, and it is why we still believe a recession lies ahead. However, history also tells us that recessions lag the inversion by approximately 18 months. The yield curve inverted in earnest last summer. Therefore, it is possible the recession could be pushed to 2024. Whatever. We think the inversion matters and it will once again precede a recession.

The chart below shows that an inversion of the yield curve (line dips below zero) has preceded each of the last six recessions (shaded area) since 1980.

Housing

Housing is where the economy, interest rates, inflation and consumer sentiment come together. The rate at which the housing market has slowed down in recent months is breathtaking. It is easy to understand what is happening, though.

First, almost every homeowner in the U.S. has refinanced their mortgage to a rate near 3%. With rates above 6%, it makes little sense for anyone to trade houses and give up their 3% mortgage in favor of a 6% rate. Second, with all the talk about a recession, there is little incentive to buy a larger home and furthermore why downsize if it comes with the higher mortgage rate mentioned above? Finally, anyone interested in buying their first home has seen prices come down from last year. Why not wait a little longer to see if rates decline, determine whether you keep your job and maybe prices come down further?

That said, we expect this weight hanging around the neck of housing to lighten up next year. We expect mortgage rates will start to ease. We think those living in their parent’s basement as they wait out the housing market storm will grow tired of these living arrangements. Albeit glacial in speed, the number of people seeking housing continues to climb and the number of homes being built is not keeping up. These factors could lead to at least a reversal of the downward spiral in housing for 2023. As all homeowners know, once you buy a new home, you tend to fill it with new stuff. It is the American Way!

Stocks

Back-to-back negative returns for stocks is rare. Since 1922, stocks have seen back-to-back negative returns only four times. This list includes 1929-1932 (Great Depression), 1939-1941 (Lead-up to US involvement in WW2.), 1973-1974 (Watergate, Gold Reserve, Vietnam), 2000-2002 (Dot com Bubble.)

A negative return for 2023 would put the 2022-2023 period among these rare events. However, it would be alone among that elite group if it were to happen because 2022 was a midterm election year. Since 1922, midterm election years have seen negative performance nine times. None of these midterm years were followed-up by another negative return for stocks. In other words, since 1922, whenever stocks were down during a midterm election year, the following year was positive for stocks. If 2023 is negative for stocks, it would be the first time this has happened in over 100 years.

Not only has every year that follows a negative midterm year been positive, it has also been some of the strongest results for stocks in any year. In the chart below, we show the midterm election years when stocks were negative along with the performance of the following year. As you can see, whenever a midterm year has been negative, it has been by an average of -13%. However, the following year has seen an average return of 25%.

| Year | Return | Following Year | Return | |

| 1934 | -6% | 1935 | 41% | |

| 1946 | -12% | 1947 | 0% | |

| 1962 | -12% | 1963 | 19% | |

| 1966 | -13% | 1967 | 20% | |

| 1974 | -30% | 1975 | 32% | |

| 1990 | -7% | 1991 | 26% | |

| 1994 | -2% | 1995 | 34% | |

| 2002 | -23% | 2003 | 26% | |

| 2018 | -6% | 2019 | 27% | |

| Avg | -13% | Avg | 25% | |

| *Source: Y Charts | ||||

To us this makes sense. The midterm election is at the end of a president’s first two years. It is during this period, especially during a first term, that they work hard to follow through on election promises. At the midterm, it is not unusual for the party that lost the presidential election to vote their party into Congress. What follows is usually a period of gridlock in Washington. Stocks tend to favor periods of gridlock because businesses and individuals do not have to contend with the next piece of legislation coming out of Washington. The politicians are too busy bickering to pass anything that disrupts economic activity. This is true regardless of the party in question!

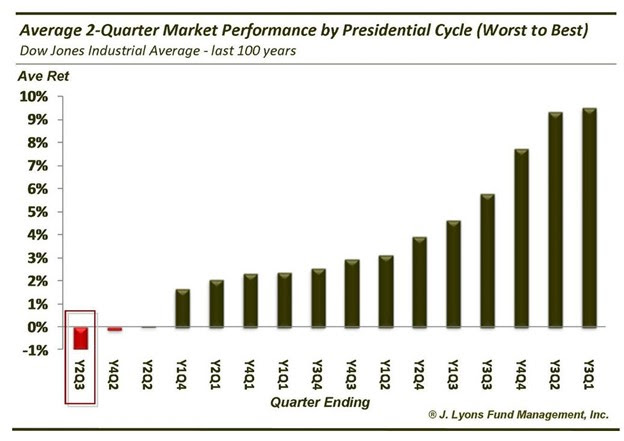

The chart below will be familiar to most readers. It shows that two of the best performing quarters for stocks have been the first two of a president’s third year in office. This points to the first two quarters of 2023.

It is also worth pointing out that two of the worst performing years for stocks are the second and third quarter of the second year. That was April through September of 2022.

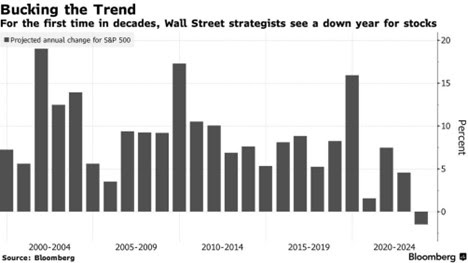

I have been a professional in this industry for more than thirty years. Only at the end 1994 and 2008 did I feel a palpable sense of negativity like I feel heading into 2023. This is nothing but an anecdotal piece of evidence, but the chart below corroborates my sense of negativity.

Wall Street analysts are known for perennially predicting a positive year for stocks. Makes sense given that positive years for stocks outnumber negative years. Even though seven of the last 22 years have seen negative stock returns (30%!), strategists have continued to predict positive results for upcoming years. Talk about sticking to your guns….

You can imagine our surprise when this year’s poll showed a change. For the first time in over twenty years, Wall Street analysts predict a negative return for stocks in the year ahead. Talk about a paradigm shift!

If you are looking for a textbook opportunity to be a contrarian, this might be it. When a group of professionals who has missed every negative year suddenly decides 2023 is the year to be negative, it is worth considering they might be wrong again.

Summary

We see all the signs of economic weakness being discussed in the media. A recession is ahead even if it comes later in 2023 or 2024. The inverted yield curve tells us so. The Federal Reserve will continue to hike rates after the first of the year and could easily raise them too much for the economy to handle. Such an overstep would send the economy into a recession and we could face another year of negative results for stocks. Inflation is not fully under control and could turn into stagflation if growth faulters. The war in Ukraine continues and we are not all the way through a dangerous winter for Europe.

The list of risks to markets is long….but that is not unusual. From geopolitical, to economic, to policy driven. This risks are also readily apparent. They have been largely discounted by stocks and bonds. The bond market will offer stability in 2023 instead of contributing to volatility like it did in 2022.

There are many strategists we respect who are predicting another year of negative returns for stocks. We do not lean in the opposite direction from their outlook just because we want hope for positive returns or because we want to lift the spirits of our clients. We do so out of discipline. A discipline to be thoughtfully contrarian and not contrarian out of spite or laziness.

There are forces that could lead to another year of negative results for stocks, but those forces are not the blips on the radar that we can plainly see. They are exogenous and ever-present forces even during the best-performing years for stocks. We cannot fear investing just because of these hidden and ever-present threats. If we did, we would be doing our clients a disservice.

So, while we acknowledge stocks could see rocky days ahead, we wax bullish heading into 2023. We are cutting against the grain of bearishness but rely on our experience and depth of research in doing so. We have outlined our case for being bullish on stocks but remain alert for signs we are off base. We will tac the sails of our investment strategies to the prevailing winds of the market. We never forget that it is hard-earned life savings that we are acting as stewards of for clients.

From all of us at KIG, we wish you the Happiest of Holidays and a prosperous New Year.

PAST PERFORMANCE DOES NOT PREDICT FUTURE RESULTS.

Sincerely,

Kessler Investment Group, LLC

All information in this presentation is believed to be from reliable sources; however, we make no representation as to its completeness or accuracy. All economic performance data is historical and not indicative of future results. The market indices discussed are unmanaged. Investors cannot invest in unmanaged indices. Certain statements contained within are forward looking statements including, but not limited to, statements that are predictions of or indicate future events, trends, plans or objectives. Undue reliance should not be placed on such statements because, by their nature, they are subject to known and unknown risks and uncertainties. Please consult your adviser for further information.

Opinions shared in this presentation are not intended to provide specific advice and should not be construed as recommendations for any individual. Please remember that investment decisions should be based on an individual’s goals, time horizon, and tolerance for risk.